Sunbathing, China supports the "report card" of the United Nations cause.

At the invitation of Foreign Minister Qin Gang of China, Korosi, President of the 77th UN General Assembly, visited China from February 1 to 4.

Kohler Heezen commented on China’s contribution to the cause of the United Nations: China has always been the strong backing of the cause of the United Nations and played an important role in the fields of climate change and peacekeeping.

As a permanent member of the United Nations Security Council and the first country to sign the Charter of the United Nations, China has always defended the purposes and principles of the Charter, always safeguarded the central role of the United Nations in international affairs, and unswervingly worked as a builder of world peace, a contributor to global development and a defender of the international order. By combing the relevant facts and data, people can see China’s clear and remarkable "report card" for supporting the United Nations cause.

The United Nations Headquarters Building in new york.

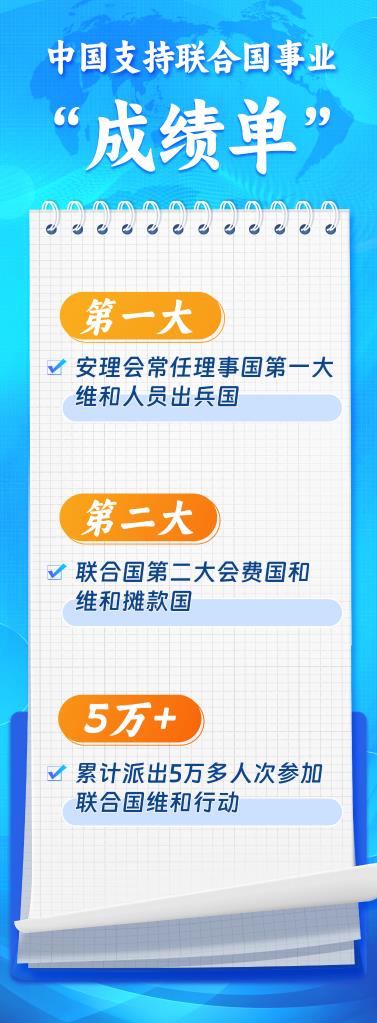

The key force of global peacekeeping

The United Nations, founded at the end of World War II, bears the expectations of people of all countries for permanent peace. However, Chinese civilization has always advocated "building a harmonious country", "harmony is different" and "harmony is the most important thing" to maintain peace and stability. China and the United Nations share the same ideas.

In today’s world, conflicts continue and various security challenges emerge one after another. In April 2022, the Chairman of the Supreme Leader put forward the Global Security Initiative at the Boao Forum for Asia, stressing that mankind is an inseparable security community, contributing China wisdom to make up the peace deficit of mankind, and providing China’s solution to international security challenges, which won wide recognition from the international community, including the United Nations.

Actively participate in the political settlement of hot issues in major regions such as the Korean Peninsula nuclear issue, the Iranian nuclear issue, Afghanistan, Myanmar, Palestine and Israel; Efforts should be made to safeguard the authority and unity of the Security Council and support the United Nations in providing good offices in accordance with its mandate; Actively participate in the international arms control and disarmament process and join dozens of international arms control treaties and mechanisms such as the Treaty on the Non-Proliferation of Nuclear Weapons; On the Ukrainian crisis, China has always decided its position and policy according to the merits of the matter itself, upheld an objective and fair position, and actively persuaded and promoted talks … … China shares security with the world and injects positive energy into world and regional peace and stability.

Former UN Secretary-General Ban Ki-moon said that China is committed to being a builder of world peace, a contributor to global development and a defender of international order, which is consistent with the ideals enshrined in the UN Charter.

Power source of global development

"In the face of the severe impact of the epidemic, we should jointly push global development towards a new stage of balance, coordination and tolerance. Here, I would like to propose a global development initiative. " In September 2021, the Chairman of the Supreme Leader put forward the global development initiative for the first time at the general debate of the 76th session of the United Nations General Assembly.

Adhere to development priority, people-centeredness, inclusiveness, innovation drive, harmonious coexistence between man and nature, and action orientation — — China’s proposition aroused warm response from the world, and China’s action promoted world development and progress.

Today, the global development initiative has achieved a series of early gains: the establishment of the global development promotion center, and the invitation of the "Group of Friends of the Global Development Initiative" countries, regional organizations and relevant departments of the United Nations to designate corresponding institutions to establish the "Global Development Promotion Center Network", which has been joined by counterparts from 31 countries and regional organizations; A global development project library has been established. The first batch of 50 projects have been started, and now more than 100 projects have been expanded, and 1000 human resources training sessions have been carried out, covering more than 50 "friends group" countries.

In the past ten years, the "One Belt, One Road" initiative has also become a popular platform for international public goods and international cooperation, covering two-thirds of countries and one-third of international organizations.

Natalia Kanem, Executive Director of the United Nations Population Fund, said that with the global population exceeding 8 billion, China’s development and contribution will benefit many countries in the world.

The biggest contributor to global poverty reduction

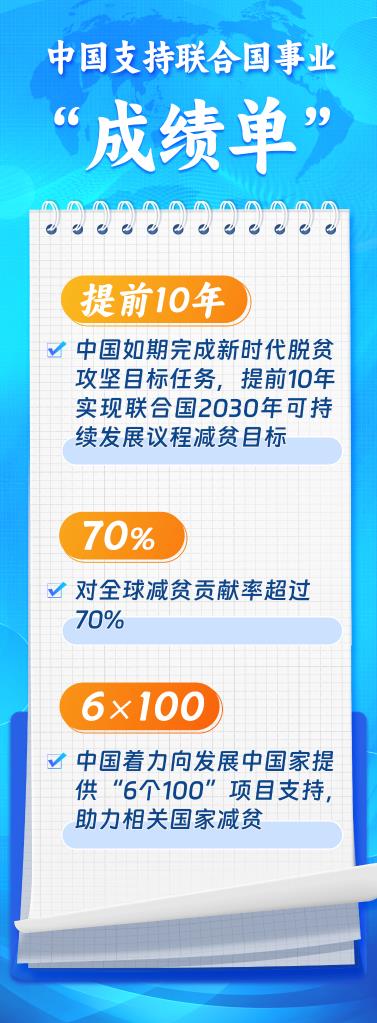

"China has solved the problem of food and clothing for more than 1.3 billion people and lifted more than 700 million people out of poverty, which is a major contribution to the cause of human rights in the world." In January 2017, when the Chairman of the Supreme Leader delivered a keynote speech at the UN headquarters, he pointed out the world significance of poverty reduction in China.

In December, 2020, China officially announced that after eight years of continuous struggle, China had completed the goal and task of tackling poverty in the new era as scheduled. Under the current standards, all the poor people in rural areas were lifted out of poverty, and all the poverty-stricken counties were stripped of their hats, thus eliminating absolute poverty and regional overall poverty and achieving a major victory that made the world sit up and take notice.

Poverty is a chronic disease in human society, and anti-poverty has always been a major event in governing the country and safeguarding the country at all times and in all countries. Facing the global governance problem of poverty eradication, China has never hesitated to share its experience and contribute to international poverty reduction while achieving its own poverty reduction.

In recent years, China has made great efforts to provide "six 100" projects to developing countries, including 100 poverty alleviation projects, 100 agricultural cooperation projects, 100 trade promotion assistance projects, 100 ecological protection and climate change response projects, 100 hospitals and clinics, 100 schools and vocational training centers, to help the countries concerned reduce poverty.

In the Asian region, China has implemented the demonstration cooperation technical assistance project for poverty reduction in East Asia in rural communities in Laos, Cambodia and Myanmar; In Africa, China has built water conservancy infrastructure for African countries, built a demonstration zone for agricultural cooperation, and promoted the implementation of projects such as technical cooperation between China and Africa; In the South Pacific region, carry out technical cooperation and assistance projects such as infrastructure construction and agricultural medical care; In Latin America, build agricultural technology demonstration centers to help local people in recipient countries get rid of poverty … …

UN Secretary-General Guterres said that China is "the country that has made the greatest contribution to global poverty reduction".

Unite the practitioners who fight the epidemic.

"People from all countries watch and help each other, showing the courage, determination and care of mankind in the face of major disasters, and illuminating the darkest moment. The epidemic will eventually be defeated by mankind, and victory will surely belong to the people of the world! " In September, 2020, when the COVID-19 epidemic was raging repeatedly around the world, the speech made by the Chairman of the Supreme Leader in the general debate of the 75th United Nations General Assembly was inspiring.

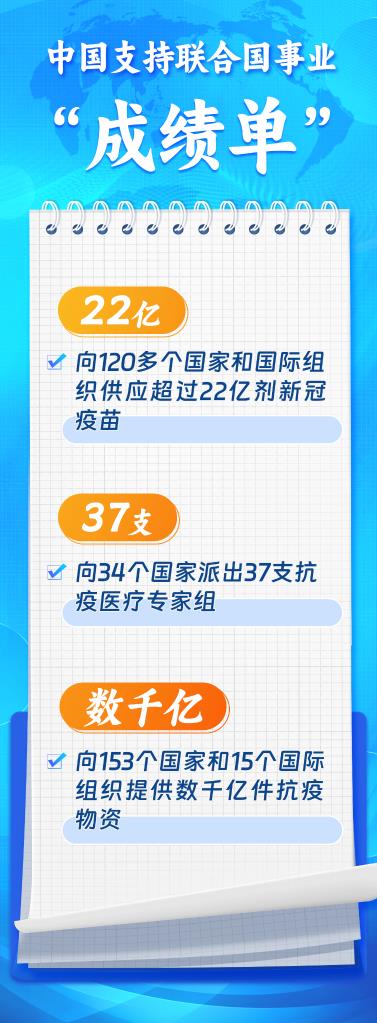

Since the outbreak of the COVID-19 epidemic, China has been helping each other with the rest of the world, sharing anti-epidemic experience in time, rushing to help other countries with anti-epidemic materials, and actively carrying out international anti-epidemic cooperation. China has provided anti-epidemic materials to 153 countries and 15 international organizations, and co-organized more than 300 technical exchange activities such as epidemic prevention and control and medical treatment with more than 180 countries and regions and more than 10 international organizations around the world.

China was the first country to promise the new crown vaccine as a global public product, to support the exemption of intellectual property rights in vaccine research and development, and to cooperate with developing countries in vaccine production, which injected a strong impetus into bridging the global "immunization gap". China actively played the role of traditional Chinese medicine, held more than 100 video exchanges and live broadcasts of anti-epidemic experts, introduced the diagnosis and treatment schemes of traditional Chinese medicine to more than 150 countries and regions, and provided traditional Chinese medicine products to some countries and regions in need.

Romina Sudak, a member of the Argentina Research Group in China, Rosario University, Argentina, said that China has helped developing countries to fight the epidemic, and China has implemented its consistent concept of "community of human destiny" with practical actions.

The doer of green development

"The sky goes at four o’clock without words, and everything is alive without words." China is an active advocate and a down-to-earth doer in tackling climate change and strengthening global environmental governance.

Chairman of the Supreme Leader has repeatedly expounded China’s proposition of building a clean and beautiful world and protecting the beautiful home of the earth on United Nations occasions. "Lucid waters and lush mountains are invaluable assets. We should follow the concept of harmony between man and nature and seek the road of sustainable development. "

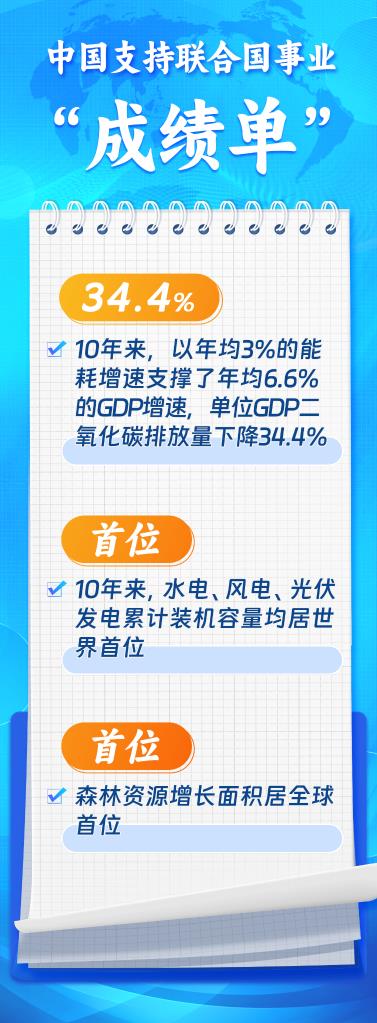

Make a historic contribution to the conclusion and rapid entry into force of the Paris Agreement, take the lead in issuing the National Plan for China to Implement the 2030 Agenda for Sustainable Development, fully implement the United Nations Framework Convention on Climate Change, announce the timetable and road map for achieving peak carbon dioxide emissions and carbon neutrality, and introduce the "1+N" policy system for implementing the dual-carbon goal, leading the world in the field of renewable energy development, becoming the country with the greatest contribution to the global ozone layer protection, and making green practical. … As the largest developing country, China promotes the construction of a community of human and natural life with consistent determination and strong measures, and contributes to the protection of human common home and the realization of human sustainable development.

Simon Steele, Executive Secretary of the Secretariat of the United Nations Framework Convention on Climate Change, said that at present, the international community is facing an energy crisis, and China has made substantial progress in the field of climate change and played an important role in promoting the global response to climate change.

At present, the world is standing at the crossroads of history. The changes of the world, times and history are unfolding in an unprecedented way, and human society is facing unprecedented challenges. People pray for the sunshine of peace, development and progress to penetrate the haze of war, poverty and backwardness.

The road is not alone, and the world is a family. China is willing to work with other countries in the world to push the United Nations to play a more active role in the lofty cause of promoting human peace and development, to promote the common values of peace, development, fairness, justice, democracy and freedom, to safeguard world peace, promote world development and promote the building of a community of human destiny.

Planning: Ni Siyi

Producer: Feng Junyang and Mao Lei

Coordinator: Yan Junyan, Han Mo, Xie Peng.

Reporter: Zhao Yan, Bird, Qiao Jihong and Chen Shan.

Editor: Han Liang Wang Fengfeng Wang Kewen Diao Ze

Vision: onion painting

Produced by Xinhua News Agency International Department

Produced by Xinhua News Agency’s International Communication Integration Platform